For those hoping for a rebalance of the market (we confess to being in that camp) the steady progress which had been building since April has stalled. The answer to rebalancing is more supply and July delivered in spades with a rise of almost 25% more active homes for sale. The last two weeks of August reversed that trend and September has been lackluster for new listings. Currently we are not seeing any clear trends in the market, but here is a smattering of information on what we are seeing.

Demand

On the demand front, home buyers are feeling the pinch of affordability courtesy of the first half of the year which brought significantly higher prices. Sales counts (closed sales) have started to drop and are slightly lower than last month and this time last year. What is propping up demand is increased activity from all categories of investors (fix & flip, landlords, and instant institutional buyers) and second home purchasers. Michael Orr of the Cromford Report confirms this: “If it were not for the activity of investors and iBuyers, and particularly the latter, the market would have cooled during August. This would have been following the trend established since April… Demand is improving but a lot of this is coming from investors and iBuyers so could die away quickly. Demand from ordinary home-buyers is subdued, no matter what the media might be telling you. If the iBuyers stop their spending spree then demand could fall quickly.” This leads us to the topic of iBuyers.

iBuyers ( “instant” buyers: Zillow, Open Door, Offer Pad, etc.)

We have not commented about the iBuyers much lately. When they first entered the market place in 2016, the high cost to the homeseller to eliminate a few days of showings in a seller’s market did not seem to make any business sense for homesellers. But the models are ever evolving. During the initial outbreak of Covid in March of 2020, iBuyers cancelled almost all their contracts – leaving a wake of very angry home sellers. Fast forward to today, iBuyers are in a buying frenzy the likes of which we haven’t seen before. With that has come improved offer prices. Even though in most cases the consumer will make more on the open market than when taking an instant offer – we certainly understand that for some, time is more important than money. So that our clients can examine all their options but with representation, we have formed a partnership with the largest iBuyer allowing us to obtain offer (s) on behalf of our sellers at no cost/no commission to the seller.

But we digress, back to the iBuyer buying frenzy, Michael Orr of the Cromford Report further some cause for concern: … iBuyers have purchased so many homes over the last month that they are significantly distorting the market dynamics. These homes are mostly going to be re-marketed shortly so they will almost certainly increase supply over the coming weeks… the iBuyers have purchased about 2,850 homes over the last 3 months. That represents almost 9% of re-sale purchases… If iBuyers had not done this, we estimate that supply would already be higher by some 1,800 listings…. We conclude that pricing would also be weaker without their intervention. This begs the question: what happens if they stop buying on this massive scale? The market is therefore more precarious than if demand were primarily growing through owner-occupiers.” (Emphasis added)

There is valid cause for concern about how the iBuyers’ actions will impact our market. What we know for sure is this buying frenzy will not last forever.

Forbearance

Much concern has been expressed about the potential impact the expiration of the federal moratorium on foreclosures may have on our market (i.e. will a flood of foreclosures be headed our way). Any worries seem to be overblown, as we are at historic lows for foreclosures and record high equity levels for most. Add to that the continuing low inventory – and foreclosure should be last on their list of options.

Tom Ruff from ARMLS Stat explains:

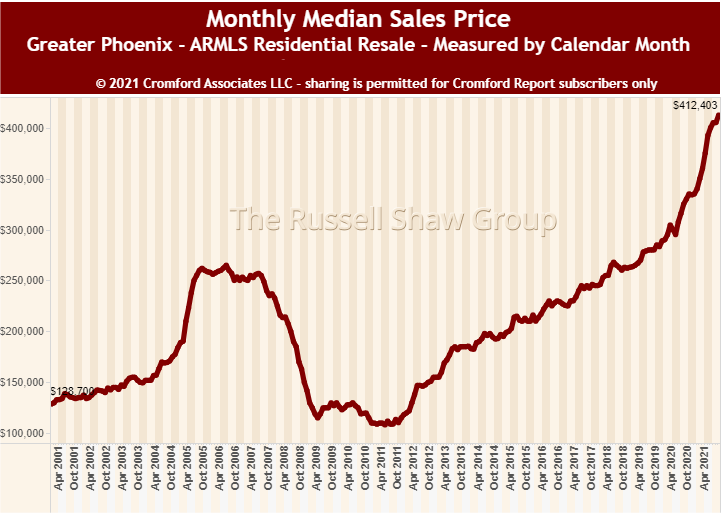

If we assume that the homes in forbearance were purchased prior to the COVID-19 outbreak in March of 2020 when the median sales price for a resale home in Maricopa County hovered around $300,000; based on today’s median of $405,000; their properties have appreciated 35% while in forbearance.

Distressed but equity rich sellers should avoid foreclosure at any cost. The market is ready to absorb them quickly at the moment.

Rental rates

Homeowners may generally be unaware the impact the rental market can have on home purchases. When it is cheaper to rent than own, people rent. When it is cheaper to buy than rent, more people own. When there is a shortage of homes for the population, both resale and rents should rise. Here are some interesting stats from Michael Orr:

“The average rental price per square foot, based on ARMLS listings, has increased from $1.00 in September 2019 to $1.36 this month. That is a 36% increase in just two years and must be a budget problem for tens of thousands of tenants. The 19 year period from September 2000 to September 2019 saw only a 28% rise, so the cost of renting has escalated over a very short period. The housing bubble of 2004-2008 saw little to no rise in rents and in fact the low point was 64 cents in February 2005, just as the for sale market was reaching its highest frenzy. This time is very different - showing that the rapid appreciation in home values is due to real shortage of housing rather than speculative activity based on easy money.

Although the cost of renting has jumped 36% over 2 years, the average home price per square foot has increased by far more - from $169.26 to $262.21 (September month to date), a jump of 55%.”

Will all these tidbits coalesce in to a trend? Time will tell. As always, we will keep you informed.

Russell & Wendy (mostly Wendy)